Quick Answer

AGM Team Last updated: May 18, 2026

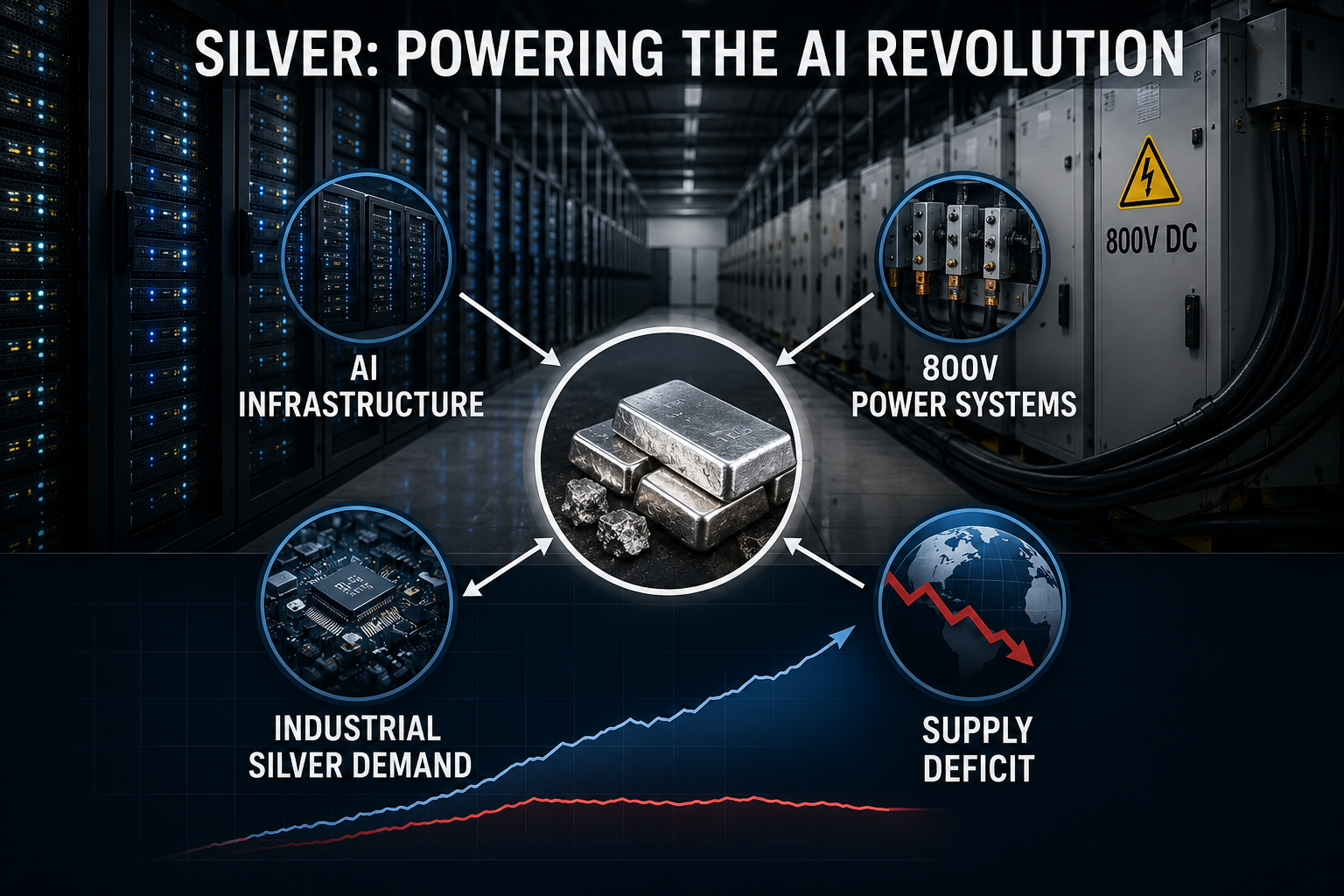

Silver is entering a structural supply squeeze driven by accelerating AI data center expansion and 800V high-voltage infrastructure. Industrial demand is rising faster than mining supply can respond, pushing the market into multi-year deficits. With inventories declining and consumption becoming inelastic, pricing is increasingly dictated by physical availability rather than traditional financial cycles.

AI infrastructure is now a structural silver consumer, while supply remains rigid and deficit-prone, creating a physical constraint pricing regime.

The Silver Market Is Entering a Physical Constraint Phase

Silver is currently trading in the $76–$86 per ounce range, while gold holds near $4,500–$4,700, keeping the Gold-to-Silver Ratio elevated at approximately 55–61:1. Despite short-term volatility and macro pressure from a firm U.S. dollar and shifting interest rate expectations, both metals remain structurally bid at historically high price levels.

Recent spot data shows silver stabilizing after a sharp multi-month expansion from sub-$75 levels earlier in 2026, with intraday pricing reaching ~$85.95/oz (May 2026) according to global bullion benchmarks.

At the same time, gold continues to trade near ~$4,600/oz, reflecting sustained macro hedging demand in an environment of geopolitical uncertainty and persistent inflation sensitivity.

Earlier in 2026, silver surged to a record high of approximately $121.6 per ounce on January 29 before entering a broader physical constraint consolidation driven by industrial demand and tightening supply conditions.

AI Infrastructure Is Becoming the New Demand Driver

This shift is occurring as AI infrastructure expands into megawatt-scale data center design, with hyperscalers accelerating deployment of next-generation compute systems. According to 2026 industry data, global data center capacity is on track to nearly double by 2030, driven primarily by AI workloads and high-density computing requirements.

The structural implication is clear: silver is no longer responding primarily to financial cycles; it is increasingly being pulled into industrial consumption tied to AI hardware expansion.

Despite macro headwinds, silver continues to demonstrate resilience near multi-year highs, signaling that physical demand is tightening faster than supply can adjust.

How AI Data Centers Depend on Silver in Core Hardware and Power Systems

AI data centers operate under extreme electrical load conditions, where efficiency losses translate directly into higher operational cost and thermal stress. As AI workloads scale across GPU clusters and high-density compute racks, silver is increasingly used as a functional conductivity and thermal optimization material rather than a discretionary input.

According to recent industry analysis of AI infrastructure materials, electronics and electrical applications already account for ~65–70% of global industrial silver demand, driven by high-performance computing, power electronics, and network infrastructure.

Server Boards and High-Speed Interconnects

Inside AI servers, data is transmitted through ultra-dense circuits connecting GPUs, TPUs, and high-bandwidth memory systems. At these speeds, even minor resistance losses can scale into measurable performance degradation across large clusters. Silver is used in:

- printed circuit board (PCB) traces

- conductive pastes and silver-filled inks

- electroplated high-reliability contacts

- SAC-type solder alloys containing ~3% silver in advanced packaging systems

Silver remains the highest electrical conductivity metal; ~5% higher than copper, making it critical for minimizing resistance in high-frequency signal pathways where latency and heat buildup directly affect system stability.

In large-scale AI deployments, thousands of such connections operate continuously, meaning performance gains per unit compound significantly at rack level.

Power Delivery and Heat Management Systems

AI workloads place heavy stress on power distribution systems and thermal management infrastructure. Silver is used in these environments because of its efficiency in both electrical conduction and heat transfer.

- Silver is used in busbars, switchgear, and contact points within power delivery units (PDUs) and backup systems.

- It helps reduce energy loss during high-load power transmission, improving overall system efficiency.

- In cooling systems, silver is incorporated into thermal interface materials and heat spreaders to move heat away from high-performance processors more effectively.

- It supports stable operation of AI systems running continuously under extreme computational loads.

The Expanding Silver Demand Inside AI Infrastructure

As AI deployment scales globally, the underlying hardware footprint expands at the same pace. Every additional server rack or data center facility increases the cumulative demand for conductive and thermal materials, including silver. This creates a direct link between AI growth and industrial silver consumption, where expansion is not theoretical but physically material-intensive.

The 100 GW Expansion Wave Is Creating a Structural Demand Floor

The scale of AI infrastructure expansion is becoming increasingly difficult for commodity markets to absorb. According to JLL’s 2026 Global Data Center Outlook, nearly 100 GW of additional global data center capacity is expected to come online by 2030, a buildout large enough to effectively double current global capacity within just a few years.

That growth carries major implications for industrial silver demand. Advanced AI facilities require large amounts of conductive and thermal materials across power distribution systems, switches, relays, circuit boards, connectors, and cooling infrastructure. Industry supply-chain estimates increasingly suggest that each gigawatt of high-density AI data center capacity may require roughly 0.5 to 1.2 million ounces of silver, depending on system architecture and power intensity.

Unlike jewelry or short-term investment demand, this consumption is tied directly to long-cycle infrastructure deployment. As AI expansion accelerates globally, silver demand becomes increasingly connected to physical compute infrastructure rather than market sentiment alone, creating a more durable structural floor for industrial consumption.

Understanding Silver Usage at Scale

At large infrastructure levels, silver demand can be conceptualized through compute capacity and hardware density. More AI models, higher training loads, and larger data center builds all translate into increased material requirements across electrical and cooling systems.

This makes silver consumption not random or speculative, but structurally tied to the physical expansion of AI infrastructure itself.

The 800V Power Shift and Its Impact on Silver Demand

The transition toward 800V electrical architecture is becoming one of the most important infrastructure upgrades inside modern AI systems. As hyperscalers and chip companies build larger AI clusters, power efficiency is becoming as critical as compute performance itself.

According to JLL’s 2026 Global Data Center Outlook, global data center capacity is projected to nearly double to 200 GW by 2030, driven largely by AI workloads and high-density computing expansion.

At the same time, modern AI racks are operating at dramatically higher power densities than traditional cloud infrastructure, forcing operators to redesign how electricity is delivered, cooled, and managed inside data centers.

Why 800V Architecture Matters

800V systems operate at higher voltage levels than traditional electrical setups, allowing the same amount of power to be delivered with lower current. Using basic electrical principles, lower current reduces:

- heat generation

- transmission losses

- cable bulk

- cooling pressure

Recent industry implementations show that 800V HVDC designs can eliminate multiple AC-to-DC conversion stages, improving overall energy efficiency by up to ~5–12% while simplifying infrastructure complexity.

JLL estimates AI workloads could represent nearly 50% of global data center activity by 2030, compared to roughly 25% in 2025.

As rack densities rise and inference workloads expand globally, higher-voltage systems are becoming necessary for maintaining efficiency at scale.

Why Higher-Voltage Systems Increase Silver Usage

Higher-voltage infrastructure places greater stress on switching points, thermal interfaces, and power-delivery components. This increases the importance of highly conductive materials like silver in critical system nodes.

Silver is increasingly used in:

- high-load connectors and busbars inside PDUs

- switching and relay components handling elevated voltage loads

- silver-plated interfaces for stable conductivity

- thermal materials used in liquid-cooled AI systems

This is especially important as modern AI accelerators move toward extremely high power consumption levels. Nvidia’s latest-generation AI platforms are already pushing GPU power requirements beyond 1,000 watts per unit in advanced training environments, significantly increasing cooling and power-delivery demands.

Why AI Demand for Silver Is Less Price Sensitive

For hyperscale AI infrastructure projects, silver represents a very small portion of total deployment costs compared to GPUs, networking systems, power infrastructure, and facility construction.

JLL estimates the global AI-driven data center buildout could require close to $3 trillion in infrastructure and equipment investment by 2030.

In that environment, the cost of silver becomes relatively insignificant compared to the operational risks of power inefficiency, overheating, or hardware instability. That makes industrial AI demand for silver increasingly price inelastic, where reliability matters more than raw material cost.

Silver’s pricing structure is increasingly driven by industrial consumption rather than financial positioning. Because silver serves both as a monetary asset and a critical industrial input, marginal demand from technology infrastructure now has a disproportionate impact on physical availability. As AI-related consumption becomes a larger share of total demand, traditional price elasticity weakens, meaning supply constraints translate more directly into sustained price support rather than cyclical correction.

Why Silver Supply Is Struggling to Keep Up

Silver supply remains constrained even as industrial demand accelerates. Global production is heavily concentrated in a few countries, including Mexico, Peru, China, and Australia, while mining growth has stayed relatively flat in recent years despite rising consumption.

Recycling helps offset part of the shortfall, but recovering silver from electronics and industrial waste is expensive and technically difficult because the metal is often used in very small quantities.

Expanding supply is also a slow process. Lower ore grades, rising extraction costs, and long mine development timelines limit how quickly new production can enter the market. As a result, the silver supply chain has become increasingly inflexible at a time when AI infrastructure and high-voltage systems are driving sustained industrial demand.

The Silver Market Has Entered a Multi-Year Deficit Cycle

The global silver market is projected to remain in structural deficit for a sixth consecutive year in 2026, according to the latest World Silver Survey published by the Silver Institute and Metals Focus. Current estimates place the 2026 shortfall at approximately 46.3 million ounces, up 15% from the previous year.

Since 2021, more than 760 million ounces of silver have been drawn from above-ground inventories to close the gap between supply and demand. Analysts increasingly describe the market as operating in an “era of reduced stocks,” where tighter physical availability can amplify price volatility and supply-chain pressure during periods of stronger industrial demand.

Where Silver Demand Is Coming from and How It’s Changing

Silver demand is not coming from a single source. It is spread across industrial use, consumer products, and investment markets. What’s changing now is the weight of each segment, especially with new technology adding a fresh layer of demand pressure.

How Silver Is Used Across Different Sectors

Silver has been used in industry for a long time, but not all sectors are growing in the same way.

- Industrial use: Solar panels, electronics, brazing materials, and automotive components still account for a major share of demand.

- Jewelry and photography: These areas are either stable or slowly declining compared to the past.

- Investment demand: Physical silver bars, coins, and ETFs continue to attract investors during periods of uncertainty.

Taken together, industrial applications remain the core driver, while traditional consumer uses are becoming less dominant over time.

AI and 800V Systems Are Changing the Demand Picture

A new layer of demand is now emerging from AI infrastructure and advanced power systems.

AI data centers are expanding quickly as companies scale large computing models. At the same time, the shift toward 800V electrical architecture is increasing the need for high-efficiency conductive materials. Both trends rely on components where silver plays a functional role.

Forecasts from industry reports suggest that AI infrastructure growth and high-voltage system adoption are accelerating at a much faster pace than traditional industrial sectors. While older demand drivers remain important, this new wave is adding structural pressure on silver consumption.

Why This Shift Matters for the Market

The key point is not just growth, but change in structure. Historical demand was driven mainly by solar, electronics, and industrial manufacturing. Now, AI systems and advanced power networks are becoming additional demand engines on top of that base.

This creates a situation where demand is not only increasing, but also becoming more concentrated in high-tech infrastructure. Monitoring AI expansion plans and the adoption of 800V systems gives a clearer signal of where future silver consumption is heading.

The Growing Gap Between Silver Supply and Real-World Demand

The silver market is now showing a widening imbalance between what is being produced and what is being consumed by industry. Unlike past cycles where supply could adjust over time, current demand growth is being driven by AI infrastructure and advanced power systems that require immediate material input. On the supply side, mining output remains relatively slow and structurally constrained.

This mismatch creates a system where demand is rising faster than supply can respond, leading to a tightening market condition that becomes more difficult to correct each year.

What the Numbers Suggest About the Coming Deficit

Based on forward-looking projections from industry research frameworks, silver demand is expected to increase steadily through the decade, while supply growth remains limited.

- AI and 800V-related demand expands rapidly as data center buildouts scale

- Investment demand remains sensitive to macro conditions but adds additional pressure during uncertainty

Over time, total demand is projected to move further ahead of supply, creating a persistent structural deficit rather than a short-term imbalance. The widening gap reflects both rising technological consumption and the physical limits of mining expansion.

What Happens When Demand Outpaces Supply

When physical demand exceeds available supply, the effects do not stay theoretical. They show up in how the market behaves and how industries operate.

- Price volatility tends to increase as physical availability tightens

- Technology manufacturers may face longer lead times for critical components

- Large-scale infrastructure projects, including AI data centers, can experience procurement delays

- The difference between paper pricing and physical availability can widen, especially when real metal becomes harder to source

In practical terms, this means the physical market can tighten even when financial markets appear stable on the surface.

Understanding Market Stress Across Different Scenarios

Future outcomes depend heavily on how quickly AI infrastructure expands and how constrained silver supply remains.

- In a moderate growth scenario, demand rises steadily but remains manageable within existing supply structures

- In a high-growth scenario, AI and 800V adoption accelerate faster than mining expansion, increasing deficit pressure

- In a constrained supply scenario, limited substitution options and mining delays intensify physical shortages

Each scenario leads to different levels of market stress, but all point toward a structurally tighter silver supply environment if current trends continue.

China’s Export Controls Are Adding Friction to Silver Supply Chains

China plays a major role in global silver refining and processing, which gives its export policies significant influence over international supply flows. Beginning in 2026, Beijing tightened export licensing requirements for silver and other strategic materials, limiting overseas shipments to approved firms under stricter regulatory controls.

The policy does not ban silver exports outright, but it increases friction across the supply chain through licensing requirements, administrative approvals, and tighter oversight. This matters because global technology manufacturers already depend on stable access to refined industrial silver for electronics, AI hardware, and power systems.

In a market already facing structural supply deficits, additional trade and refining bottlenecks can further tighten physical availability and increase procurement costs across industrial sectors.

This friction is occurring precisely as AI infrastructure and high-voltage 800V systems increase global dependence on refined silver inputs, amplifying the impact of any supply-side bottlenecks.

What the Silver Supply Squeeze Means for Investors

Silver is no longer just a traditional precious metal. With rising demand from AI infrastructure and 800V power systems, it is increasingly viewed as an industrial input tied to long-term technology growth. This changes how investors think about it, not as a short-term trade, but as a structural exposure to future demand trends.

How Silver Fits into a Long-Term Investment View

In this environment, short-term price moves matter less than underlying fundamentals. The key focus shifts to:

- persistent supply deficits

- rising industrial usage from AI systems

- limited ability of mining supply to respond quickly

The real evaluation is not just price direction, but how tight the physical market becomes over time. Investment decisions are more aligned with long-term technological adoption rather than short-term volatility.

Main Ways to Get Exposure to Silver

Different investment routes behave differently when supply is tight:

| Investment Type | Key Benefit | Key Limitation | Risk Level |

| Physical silver (bars/coins) | Direct ownership, no counterparty risk | Storage and higher premiums | Lower–moderate |

| Silver ETFs | Easy access and liquidity | No direct metal ownership | Moderate |

| Mining stocks | Leverage to silver price moves | Company and operational risk | Moderate–high |

| Futures/options | High leverage opportunities | Very high complexity and risk | Very high |

What Actually Matters When Evaluating Options

In a supply-constrained market, the focus should be on exposure quality, not just product type. Key points to assess:

- physical vs paper exposure

- storage and security for physical holdings

- premiums and market spreads during tight supply conditions

- overall diversification across different exposure types

The Dip May Be the Opportunity

AI infrastructure is now a structural silver consumer, while supply remains rigid and deficit-prone, creating a physical constraint pricing regime.

Silver is no longer behaving like a conventional macro-driven commodity. As of May 2026, prices remain elevated in the $75–$86 range, with gold near $4,500–$4,700, and a persistently high Gold-to-Silver Ratio around 55–61:1 reflecting ongoing imbalance in relative valuation rather than short-term sentiment.

What defines the current phase is not price direction, but physical constraint under industrial acceleration. Multiple years of structural deficit, estimated at roughly 46 million ounces in 2026 alone, combined with steady depletion of above-ground inventories, has reduced the system’s ability to absorb demand shocks.

At the same time, AI infrastructure expansion, high-density computing deployment, and 800V power system adoption are embedding silver directly into next-generation electrical and thermal architectures. This demand is not cyclical; it is tied to long-duration infrastructure buildouts that cannot be quickly reversed or substituted.

In practical terms, silver is transitioning into a material where industrial consumption is increasingly dominant over financial positioning, reshaping how price stability forms across cycles.

The result is a market where traditional macro signals matter less than physical availability. In this environment, volatility is not random; it is a reflection of tightening supply conditions meeting persistent structural demand.